Stress-Free Business Account Setup For Small Business Owners

Have you had problems setting up a business bank account? In this blog, we will share our experience when we were setting up our business account a couple of years ago. Lessons learned from our own experience, that shared by our clients, our research and new technology.

Two years ago, we couldn’t wait to set up our business. We thought the last thing we will need to worry about is my business bank account. We were wrong, it took me almost 3 weeks to finally get the bank account to go live. Not sure if that was the norm but it was a bit frustrating, you won’t believe it but the bank misplaced our application form. Fortunately, because of our line of work other business owners have shared similar experiences with us. We have constantly come across clients who have been through far worse experiences. Maybe the tree weeks experience wasn’t so bad. Phew!

Traditional Banks

The banking sector has gone through a lot of changes since the 2008 recession. Most banks had to write off their subprime bad debts on their balance sheets. Eleven years down the line some banks are still recovering from the repercussions of 2008. We can not forget that most of our household banks’ almost went burst. For small businesses, access to business loans banks was a real issue and still in certain circumstances. Banking fees have eaten into small business profits, especially, the small businesses that predominantly deal with cash deposits and cheques. Small businesses heavily reliant on cash deposits, normally incur bank fees depending on the volume of cash and cheque deposits. They need security to transport their cash to the bank and this comes with an added cost.

Digital Products Disrupting the market

Western economies are moving towards a wholly digital environment. Plans by banks’ to phase out cheques by the end of 2018 in the UK did not come to fruition, banks had to retreat after intervention by MPs.It is understandable why traditional banks’ (Barclays, HSBC, NatWest etc) were vying for the extinction of cheques. If you have ever been exposed to the chaos in the UK cheque clearing system you will appreciate the level of threat posed by fraudsters. Despite the advancement in optical character recognition (OCR), the technology is still nowhere perfect when it comes to recognising handwritten cheques. The reason is obvious, you may need to be a qualified optician to read some handwritten cheques. The level of risk for small businesses highly reliant on cash and cheque deposits are very high. The day to day exposure to the operational risks of fully disclosing cash is also high. Small Businesses can put in place measures like electronic card payments system to reduce their exposure to cash and cheques.

Unlike previous stringent contracts accompanying card terminals, there is no need to have such stringent contracts if you don’t want to. Most of the disruptive card providers work on a pay as you use agreement. You only get charged a percentage per the value of your transaction. No transaction, no fee. It’s as simple as that and a lot more transparent. Card terminals are a lot cheaper now, averaging at £30, no need to rent them for monthly fees. Payment received via the credit terminals get credited to your business accounts in about 3 working days. This is one of small business’ answer to reducing their risk of over-reliance on cash. The new disruptive terminals can be carried anywhere using mobile data without extra cost.

A couple of terminals and how they work, these can be carried around anywhere. If you need our help to make a decision, please contact us and we will do well to help.

Meaning and Evolution of Fintech

Online banking was first introduced in the 1980s in New York according to Wikipedia. There has recently seen the influx of Finance technology and they have started disrupting the banking industry. Fintech is a combination of using financial tools and technology to provide financial services.

According to an Evolution of Fintech article by Forbes, the Fintech framework has been in existence since the 1950s, with the introduction of credit card payments through to online banking. The term has become popular with internet payments, mobile payments apps like Apple pay, and PayPal. Earlier disruptions were predominantly associated with the influx of additional financial and technology tools which complemented existing traditional banking services. Forbes research indicates that the term started emerging from 2015. However, what is different now is the complete startup of the whole Fintech business model. This has been posing as a real competition risk for traditional banks, who in the past have been dominant in the banking sector. These banks’ have had complete influence on government policies and regulations. After all most of the Government’s financial regulators are poached from the same traditional financial and banking institutions. This made sense because they understand the sector better, as well as the loopholes that existed. It is a relief to see the regulators giving Fintech startups a chance to compete with traditional banks. However, there is also the worry that the Fintech business model is new to regulators and they may be trying to understand as well as catch up. Despite any foreseeable challenges, the initial benefits look promising for consumers.

Real Test

Traditional banks’ have struggled to get to grips with the recent technology disruptions, unlike previously complemented tools, this time the disruptors are sidelining traditional banks’ and going it alone. Earlier financial service disrupts on funding platforms and venture capitalists paved the way for Fintechs to raise huge amounts of capital from other sources other than the traditional banks’, thus preventing the banks’ from getting insight about the business plans of the disrupts as well as allowing the traditional banks to have a stake in them. Fintechs have found backing from unfamiliar sources. This has given them the platform to alienate traditional banks’ as well as pose as a real threat. For the consumer, this is very good news. Customers, especially those between the ages of 18 to 30 years needs are being met. They can access their financial data on their mobile phones, pay for products and services through their apps. Core needs of the consumer are being profiled leading to practical delivery of targeted services. Costs borne by the consumer is lower or completely non-existent.

Challenge for traditional banks to Catch up

Like most recognised brands and companies, traditional banks’ spent a fortune on legacy systems which are were located in-house and with a huge budget because they could afford it. The legacy systems require highly skilled staff to maintain them as well as keep up with the security of the databases. Fintechs have the advantage of leasing cloud storage spaces. This leased cloud storage comes with the expertise, skills and the security to keep scammers at bay. This doesn’t mean the systems pose no security risks. No one knows what is around the corner or the existing loopholes that exist in cloud technology. Most developers and manufacturers are new to cloud technology. It is humans who develop the software to protect the cloud storage and the same people can move to the other side of the fence and pose as a threat. However, research has shown that the security risks posed by in-house databases are higher than some advanced cloud spaces that have emerged in recent times. Some banks’ have made the effort of transferring their legacy systems into Fintech ready systems but the transfer has been fraught with its own challenges. TSB bank struggled during that transition, with customer balances mapping into the wrong bank accounts. Moving data from one technology to another is by no means an easy task. One of the main problems is, many a time the goal of the IT engineer is totally different from that of day to day end user, in this case, the finance expert. Striking a balance in order to achieve a similar goal can be a challenge. Some objectives need to be prioritised.

Efforts to get around some of the Issues

The challenges faced by traditional banks’, have encouraged them to come up with strategies to help them set up their own Fintechs on the side without it affecting their legacy system or associating it with their day to day operations. In the past traditional banks’ would have been part of Fintech startups by financing them. They also had opportunities taking a stake in the business through funding. Now that they have to do it alone they may not have the foresight and the drive that these startups have. It is also difficult to do away with the traditionally embedded banking culture unless they develop a strategy to completely make their Fintechs autonomous and that is a difficult one to run past the shareholders. Their strategy to have their own Fintechs is a step forward and better than doing nothing. They could do more by first understanding why they exist in the first place and then understand their customer needs. They already have ownership of vast amounts of customer data. In one recent TV advert, Nationwide building society mentioned that they had 15 million customers. They need to invest in analysing customer behavioral patterns and project the future patterns of customers. With access to technology, they can gradually start by moving customers data into their new Fintech startups. They could profile their customers, move them depending on their age or level of technology usage and knowledge. Sorting the banks’ legacy data can be a step forward to tackling the main driver for the change.

Easy setup process of Fintech bank accounts

In the UK and Europe, the main disruptors of Fintech banks have been Revolut, Monzo and Starling. In our recent business bank account set up we spent less than 10 minutes setting up a business account with Starling bank. The process was seamless and practical, I knew straight away this will turn traditional retail banking right on its head. The process starts with getting the app from the Apple or Android app store. The starling app is fresh and easy to follow. It searches through the API of companies house for the name of the limited company. By default, it fills in the director’s name. You are only required to answer 3 personal questions and then your personal data section is complete.

Modern ID check

Through the phone’s camera, it asks you to record a video message, what you are meant to say pops up so you do not need to waste any time worrying about that. Your picture ID is next, this is taken using your phone camera. You will be walked through each step without the need to think about it. Very user-friendly.

The last but one process is choosing your password and pin number. The very last task is to answer questions about your business projected financial data for the year. The icing on the cake is seeing your sort code and account number within a minute of signing up. Meaning you could literally start trading with your business bank details after setting it up in less than 10 minutes. Amazing news for small businesses! We have truly come a long way.

The Beauty of Fintech’s seamlessness

The whole process is done without any complexity. Compare this with our experience of setting up a business bank account a couple of years ago and you will understand why traditional banks’ are in real trouble. AI technology and the availability of technological infrastructures will lead to a disruption of many traditional businesses, this is just one-industry, there are many more to come.

Conclusion

It is only a matter of time for most industries to be disrupted. We have seen this in travel (Uber), Leisure (Internet & Airbnb), Retail (Amazon), Banking (Fintech), to name a few. One thing that is common in all these disruptions is, they have happened at the back of other technological advancements that never existed.

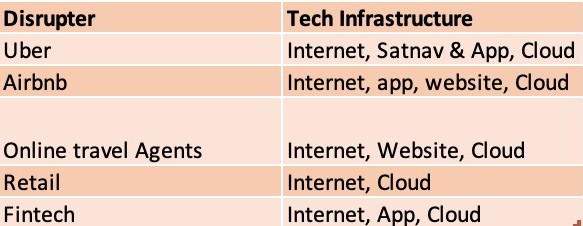

A table of some disrupting companies and their technological driving force

It is clear from the above table that the cloud infrastructure, similar to internet technology has been the main driving force to most of the disruptions we see today. Without this infrastructure being cheaply available the disruptors would have struggled to make headwinds not just financially, but logistically it would have been a nightmare.

Note that we are by no means ignoring some groundbreaking technologies that have driven the cloud technology and still drives it to the level of advancement we experience today. All businesses must be hopeful and be cautiously on the lookout. Make room for technological flexibility and scenario planning, be ready to compete against some disrupts. In most industries, there is enough demand for existing businesses to survive. Whether you are in the business of building a product or providing a service, it comes down to giving value to the customer and satisfying their needs in the long run. Starling bank allowed us to spend less than ten minutes when setting up a business bank account, that gave us ample time to go about our normal business activities, without having to worry about when we will be hearing back from the bank. How can your business save your customers time or money?

If you have enjoyed reading, please leave a comment. Leave a comment if you had a similar experience or something you read resonates with you. Whatever it is we would like to hear from you. We specialise in Business Advice and Technology advice(Biztech). Get in touch and let’s talk soon.

Stay Safe & Blessed!

Joseph Nsiah

Leave a Reply

Want to join the discussion?Feel free to contribute!